Let’s be honest for a moment: nobody likes thinking about car insurance until they hear that sickening crunch of metal on metal.

In that split second, your mind races. Is everyone okay? How badly is the car damaged? And then, inevitably, the financial panic sets in: How much is this going to cost me? Is my rate going to skyrocket?

If you’ve ever been with a standard, cut-rate carrier, you know the drill. You pay your premiums faithfully for years, have one bad day on an icy Minnesota road, and suddenly your renewal offer looks like a mortgage payment. It feels like a punishment.

At Fallon Insurance Agency, we don’t believe one mistake should erase years of safe driving. This is where the concept of Accident Forgiveness comes in—a feature that sounds great in commercials but is rarely explained in plain English.

Today, I want to pull back the curtain on what Accident Forgiveness actually does for your wallet, and while we’re at it, demystify two other “minor” features—Towing and Rental Reimbursement—that usually turn out to be major lifesavers.

The Myth of “Just Being Careful”

We talk to drivers in Cannon Falls, Rochester, and across Wisconsin every day who say, “I don’t need fancy add-ons; I’m a safe driver.”

And they are. Until they aren’t.

The reality of driving in the Midwest is that sometimes, safety is out of your hands. Black ice doesn’t care about your clean driving record. Neither does the deer that darts out on a back road at dusk. Even the most cautious driver can have a momentary lapse in judgment.

Without Accident Forgiveness, a single at-fault accident can cause your insurance premiums to surge by 30% to 50% (and sometimes more) for the next three to five years. Do the math on that. If you’re paying $1,500 a year, a 40% hike adds $600 every single year. Over five years, that one accident effectively costs you $3,000 in surcharges alone—on top of your deductible.

How Accident Forgiveness Changes the Math?

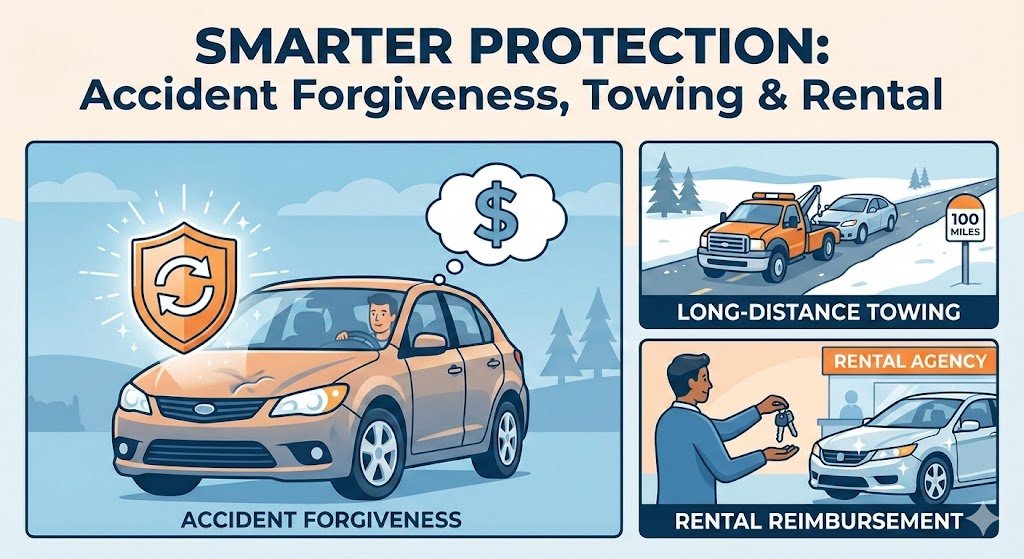

Accident Forgiveness is exactly what it sounds like: a “Get Out of Jail Free” card for your first at-fault accident.

When you have this feature on your policy with us, that first fender bender doesn’t trigger a rate surcharge. Your premium stays flat (assuming no other changes), just as if the accident never happened.

Here is why this matters for Fallon Insurance clients: We don’t just quote state minimums. We look at long-term financial health. Paying a few dollars extra per month for a policy that includes Accident Forgiveness is an investment in stability. It protects your future cash flow from the volatility of life’s “oops” moments. It’s not just about fixing your car; it’s about fixing your budget.

The “100-Mile” Difference: Why Standard Towing Fails You

Let’s switch gears to another feature that gets overlooked until you’re stranded on the side of I-94 or a rural county road: Roadside Assistance.

Most “cheap” insurance policies include roadside assistance. But have you ever read the fine print? Many standard policies cap towing coverage at 5 to 15 miles.

If you live in downtown Minneapolis and only drive to St. Paul, 10 miles might be fine. But look at where we live. If you break down outside of Cannon Falls, or you’re on a weekend trip in rural Wisconsin, the nearest qualified mechanic or body shop could easily be 30, 40, or 50 miles away.

The Scenario: Imagine your transmission blows 40 miles from home. You call your cut-rate insurance provider.

Provider: “We cover the first 10 miles.”

You: “Okay, what about the other 30?”

Provider: “That will be out of pocket. Roughly $4 to $6 per mile.”

Suddenly, you are paying $150+ just to get your car to the shop. That’s money you didn’t plan to spend, adding insult to injury.

The Fallon Standard: This is why we specifically highlight 100-Mile Towing on our auto plans. We know our territory. We know that in Minnesota and Wisconsin, “local” doesn’t always mean “close.” With 100-mile towing coverage, you have the peace of mind that we can get your vehicle back to your preferred local shop, your dealership, or your driveway, without you having to whip out your credit card on the side of the highway.

It’s a small detail on the policy declaration page, but it’s a massive difference when you’re standing in the cold waiting for a tow truck.

Rental Reimbursement: The “Hidden” Cost of Repairs

Here is a statistic that surprises most people: The average car is in the body shop for two weeks after an accident.

Supply chain issues for parts can push that to three or four weeks.

If you don’t have Rental Car Reimbursement, you have a serious problem. How do you get to work? How do you get the kids to school?

Two weeks of paying for a rental car out of pocket is $700+. That is a cost that most people forget to factor in when they are shopping for the “cheapest rate.”

How We Handle It: At Fallon Insurance, we emphasize Rental Reimbursement because it keeps your life moving. If your car is in the shop due to a covered claim, your policy steps in to cover the cost of a rental vehicle.

This coverage is the difference between a minor inconvenience (driving a different sedan for a week) and a major logistical nightmare. It allows you to maintain your routine, your job, and your sanity while the mechanics do their work.

Why “Check-the-Box” Coverage is Dangerous?

You will notice a theme here. None of these features—Accident Forgiveness, 100-Mile Towing, Rental Reimbursement—are required by state law. You can legally drive without them.

But “legal to drive” and “financially protected” are two very different things.

This is the core of the Fallon Insurance Agency philosophy. We aren’t here to give you a quote that looks good for five minutes until you realize what’s missing. We are here to build a wall of protection around your assets.

When you buy a policy online from a faceless lizard or a cartoon character, you are often getting a “check-the-box” policy. It checks the box for the state requirement, but it leaves you holding the bag for:

Is saving $15 a month really worth exposing yourself to thousands of dollars in potential costs?

The Fallon Review: Smarter Protection

We often find that when we review policies for new clients, they have gaps they didn’t even know existed. They thought they had “Full Coverage” (a term that doesn’t actually exist in the insurance world), but they really just had “Liability + Collision,” with none of the safety nets we discussed above.

Our process is different:

We Listen: We ask about your commute, your family drivers, and your financial goals.

We Educate: We explain why we recommend 100/300k liability limits instead of state minimums, and why 100-mile towing makes sense for your location.

We Bundle: By combining your Auto with your Home insurance, we can often add these premium features (like Accident Forgiveness) while still lowering your overall monthly spend compared to paying for two separate policies elsewhere.

Ready to Review?

If you aren’t sure if your current policy includes Accident Forgiveness, or if you’re worried that a breakdown would leave you stranded with a hefty towing bill, it’s time for a second look.

Don’t wait for the accident to find out what your insurance doesn’t cover.

Let’s run a custom quote. It takes about 5 minutes, and we can show you exactly how affordable real, comprehensive protection can be.

Contact Fallon Insurance Agency Today or click “Get A Quote” to start the conversation. Let’s make sure your coverage works as hard as you do.

Disclaimer: Coverage features like Accident Forgiveness, Towing limits, and Rental Reimbursement are subject to policy terms, conditions, and qualifications. Not all drivers or policies may qualify. Please consult with your Fallon Insurance agent for specific details regarding your protection.